{kind=link}

Members Hit Onerous by Weak 2022 Inventory Market – Middle for Retirement Analysis")

Extra importantly, long-run traits present little beneficial properties for median balances.

It’s at all times attention-grabbing to have a look at Vanguard’s most up-to-date version of “How America Saves.” And it’s significantly attention-grabbing to get the numbers for 2022 – not a superb 12 months for the inventory market. Certainly, the information isn’t good for 2022. Extra importantly, the longer-run traits – regardless of an amazing growth in auto-enrollment – should not very encouraging both.

Vanguard stories a considerable decline between 2021 and 2022 in each median and imply 401(okay) balances. The large distinction between the median and the typical is because of a small variety of accounts which have actually huge balances. Common balances are extra typical of long-tenured, extra prosperous individuals, whereas the median stability represents the standard participant. Imply balances dropped from $141,500 to $112,600, and median balances from $35,300 to $27,400 – declines of 20 % and 23 %, respectively, from 2021. Vanguard attributes the decline primarily to a unfavourable return on plan belongings in 2022 of -15.8 %, plus a altering mixture of individuals.

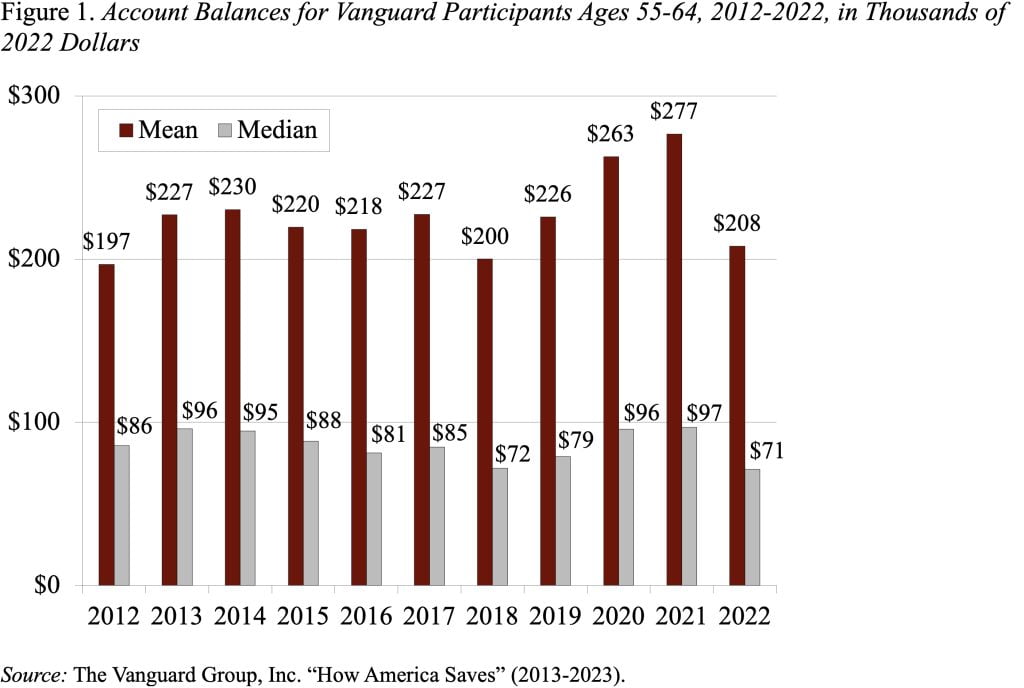

However low balances should not only a short-run downside. Balances typically are puny. Think about the holdings of these approaching retirement – ages 55-64. As one would anticipate, these balances are a lot bigger than these for the total participant inhabitants. However nonetheless the median is $71,000, which implies that half of individuals have lower than this quantity and half extra (see Determine 1). Furthermore, Vanguard tends to manage bigger plans, so the plans are higher designed than common and individuals have increased incomes. In different phrases, it presents the perfect face of the 401(okay) system.

After all, these particular person 401(okay) balances don’t inform the entire story about retirement saving. First, when individuals change jobs, their 401(okay) accounts could stay with their outdated employer, so people could have a couple of 401(okay) account. Second, 401(okay) balances could also be rolled over to an IRA, and monetary providers corporations can’t observe mixed 401(okay)/IRA holdings. Third, by necessity, balances are offered on a person, reasonably than a family, foundation. For all these causes, we’re trying ahead to information from the Federal Reserve’s 2022 Survey of Shopper Funds, which might be launched within the fall.

However assume that the median 401(okay)/IRA holdings for households approaching retirement grow to be twice the Vanguard quantity for particular person individuals – a ratio in step with earlier years. That will imply {that a} family 55-64 with a 401(okay) would have whole 401(okay)/IRA balances of $142,000.

If a pair makes use of its $142,000 to purchase a joint-and-survivor annuity, they are going to obtain – even with at this time’s excessive rates of interest – about $745 per thirty days. Since this quantity isn’t listed for inflation, its buying energy will decline over time. Furthermore, this $745 is prone to be the one supply of retirement earnings to complement Social Safety, as a result of the standard family holds just about no monetary belongings outdoors of its 401(okay).

Furthermore, households with a 401(okay) plan are the fortunate ones. Solely about half of households within the center third of the earnings distribution have such a plan.

The underside line is that our personal sector retirement system works properly for the highest third of households, offers slightly for the center third, and presents just about nothing for the underside third. We should always be capable to do higher than that.