{kind=link}

The upper your credit score rating, normally the decrease your mortgage price. Each time I went to use for a brand new mortgage or refinance an present mortgage, my mortgage lender would first ask for my credit score rating. If I stated something decrease than a 720, they might politely inform me to look elsewhere.

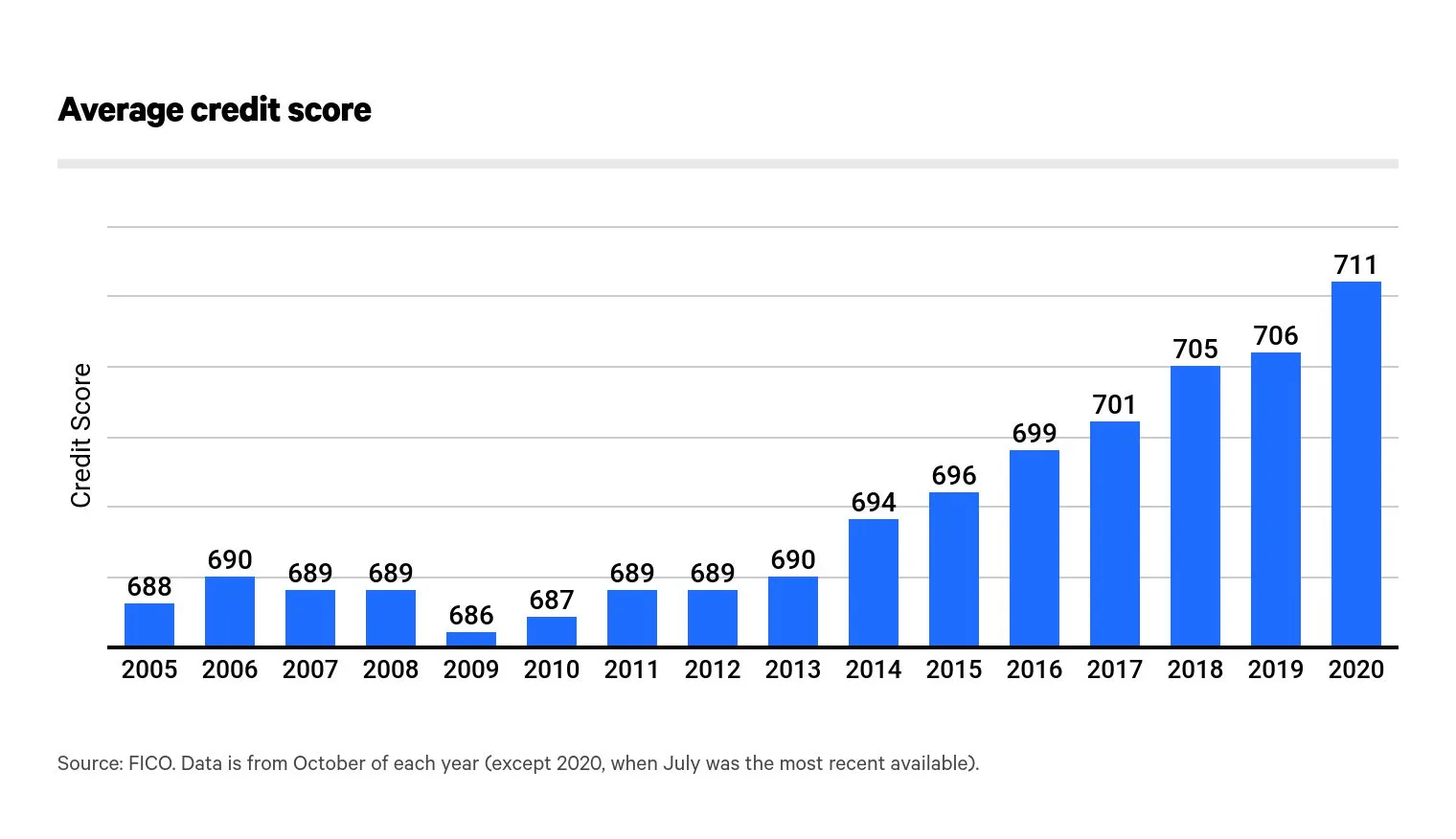

Earlier than the 2008 world monetary disaster, a credit score rating of 720 and above meant debtors might get the bottom mortgage price with the bottom charges. Nevertheless, after about 2012, to get the bottom mortgage price with the bottom charges usually required at the least an 800 credit score rating out of 850.

In consequence, I made a decision to pursue methods to get an 800+ credit score rating in an effort to get monetary savings. On September 6, 2013, I lastly broke 800 and have stayed above 800 ever since.

An 800+ credit score rating enabled me to buy a brand new property at a aggressive price in 2014. Then in 2018, I refinance the property to a fair decrease price. Extra lately, I used to be capable of purchase a endlessly house in mid-2020 with a 7/1 ARM at solely 2.125%. Being a accountable borrower has paid off.

However what if debtors with greater credit score scores needed to pay greater charges? On the margin, it might disincentivize homebuyers from being accountable debtors. In consequence, lower-credit high quality homebuyers would enter the market, thereby rising the chance of one other housing disaster.

This does not sound nice, however possibly there’s a silver lining to this perverse incentive construction.

Increased Credit score Rating Now Means Increased Mortgage Charges

The Federal Housing Finance Company (FHFA) has recalibrated the payment construction for loan-level worth adjustment (LLPA) by decreasing charges for some debtors and mountaineering these for others.

Earlier than Could 1, 2023, for instance, in the event you had a credit score rating of 740 or greater, on a $500,000 mortgage, you’ll pay a 0.25% payment, or $1,250. After Could 1, you’ll pay as a lot as 0.375% – or $1,875 – on that very same mortgage.

Paying as much as $625 extra in charges appears important. It’s a 50% enhance from what you’ll have paid earlier than the FHFA modified the principles.

In one other instance I noticed, homebuyers with credit score scores of 740 to 759 – thought-about “superb” – and placing 20% down will face a brand new LLPA of 1%, in contrast with 0.5% beforehand. For the acquisition of a $500,000 house, which means the payment doubles to $5,000 from $2,500.

Would you be OK paying $2,500 extra? I would not. Under is an instance of assorted mortgage refinance financial institution charges.

If No Increased Payment, Then A Increased Mortgage Charge

If the homebuyer is not explicitly paying the next mortgage payment, then the payment will get rolled up into the next mortgage price. The lender has to generate profits someplace. Therefore, do not be fooled by a “no-cost refinance.“

The under graphical instance reveals somebody with a 740 credit score rating paying a 0.25% greater mortgage price than somebody with solely a 660 credit score rating. A 0.25% mortgage price distinction is important.

In my expertise of aggressively buying round for mortgages, 0.25% is the most important low cost a competing lender would ever give me. And generally, I might solely get a 0.25% decrease price by transferring belongings and relationship pricing.

Decrease Credit score Rating Now Means Decrease Mortgage Charges Or Charges

If all people is getting squeezed with greater charges and better mortgage charges, then getting squeezed is less complicated to take. Nevertheless, the Federal Housing Finance Company has additionally determined to decrease the charges for individuals with decrease credit score scores.

For instance, beginning in Could 2023 a homebuyer with a credit score rating of between 640 to 659 and who has a down cost of solely 5% will incur a loan-level worth adjustment payment of 1.5%, down from 2.75%.

Which means somebody buying a $500,000 house would now “solely” pay an LLPA payment of $7,500, down from $13,750 beforehand. The unique LLPA payment of two.75% sounds egregious, so this can be a important profit for these decrease credit score rating potential homebuyers.

Nevertheless, the misplaced 1.25% in LLPA charges is now being made up by homebuyers with greater credit score scores. Folks with decrease credit score scores are both being rewarded or being given a break. Your view depends upon your philosophy.

Mortgage Originations By Credit score Rating

Absolutely the proportion enhance in charges greater credit score rating debtors will now pay is not as nice as absolutely the proportion lower in charges decrease credit score rating debtors can pay. Nevertheless, the distinction ought to be made up by quantity.

Folks with greater credit score scores make up the vast majority of debtors.

Beginning round 2010, the vast majority of mortgage originations got here from homebuyers with 760+ credit score scores. Then beginning round 1Q2020, these with 760+ credit score scores began to essentially dominate mortgage originations (mild blue bar).

The primary purpose for these modifications is tighter lending requirements after the 2008 world monetary disaster and the pandemic.

Given house costs have additionally boomed since 2010, wealth has principally accrued to these with the very best credit score scores. In the meantime, these with credit score scores beneath 660 have largely been shut out of the housing market since 2009 (yellow and darkish blue).

The federal authorities checked out this knowledge and determined to alter the payment construction within the title of equitable entry to house possession. The wealth hole between householders and non-homeowners has grown too giant.

You possibly can learn the Federal Housing Finance Company’s clarification assertion defending its new mortgage pricing.

General Implications Of Payment Adjustments Primarily based On Credit score Rating

As soon as excessive credit score rating homebuyers they have to pay this greater payment, they may negotiate tougher with their lenders to get a larger low cost. Buying round for a mortgage is at all times a good suggestion. However this additionally means there will probably be additional pressure on the lending business, which has already seen quantity dry up on account of greater mortgage charges.

When you work within the mortgage enterprise, you most likely really feel such as you’re getting kicked after you’ve got already fallen down. Rationally, lenders will begin pursuing householders with “truthful” credit score scores of 660 or much less by pitching decrease charges.

As well as, excessive credit score rating homebuyers could negotiate extra aggressively with house sellers to get worth concessions. Extra negotiating normally means longer closing occasions. Longer closing occasions usually enhance the probabilities of a deal falling by means of.

Increased charges for greater credit score rating debtors imply decrease lending and residential sale quantity on the margin. In consequence, commissions earned in the true property business will even decline. Due to this fact, I ought to add unknown new authorities laws as a threat to my optimistic actual property name for 2023.

Then once more, if the decrease mortgage charges and charges carry in additional homebuyers, then there may very well be upward strain on house costs. This, in flip, would enrich present householders even additional. And if extra individuals are richer, there will probably be much less crime and fewer pressure on the federal government to offer.

Unintended Consequence: Hurting Asian Individuals

At any time when the federal government decides to choose winners and losers, there are generally unintended penalties. This is one which I hadn’t considered.

One “unintended” consequence of getting greater credit score rating debtors to subsidize riskier debtors is the disproportionate adverse affect on Asian Individuals. I put the phrase unintended in quotes as a result of the federal government clearly sees all the information.

As an Asian American who grew up in Japan, Taiwan, Malaysia, and the Philippines for my first 13 years of life, I perceive how Asians view debt: not good. Asian Individuals are extra allergic to debt. In consequence, Asian Individuals have a tendency to save lots of extra aggressively and pay for extra issues with money.

Due to this fact, it was no shock after I discovered Asian Individuals have a median credit score rating of 745. Under is the common FICO rating by race based on the U.S. Federal Reserve knowledge. Each race will get at the least a “Good” trophy.

Mortgage Software Rejection Charge By Race

Asking safer debtors to subsidize riskier debtors who’ve largely gotten disregarded of the housing growth is one factor. Enabling extra Individuals to personal their main residence is sweet for the nation, if debtors purchase inside their means.

However what in the event you requested a bunch of people that had been experiencing greater mortgage rejection charges than the baseline White borrower to additionally subsidize this riskier group? That would appear unfair.

In line with a 2021 research by the City Institute, Asian Individuals have a decrease homeownership price (60%) than White Individuals (72%), regardless of having a greater median revenue.

One purpose for this disparity, the research discovered, is that Asian Individuals have greater mortgage denial charges than White Individuals.

“We discovered that the denial price for Asian mortgage candidates is 8.7%, in contrast with 6.7% for White mortgage candidates,” the authors of the research wrote. The authors studied the Dwelling Mortgage Disclosure Act (HMDA) knowledge.

“Asian candidates are denied extra ceaselessly than White candidates in any respect revenue ranges,” the research experiences. “In 2019, median revenue was $107,000 for Asian candidates and $82,000 for white candidates. For Asian candidates with annual incomes under $50,000, 16.3% had been denied a mortgage, in contrast with 11.3% of White candidates in that revenue bracket.”

Why Are Asians Getting Rejected At A Increased Charge Than Baseline?

No person is aware of the precise purpose why Asians are rejected at the next price for mortgages as a result of the research additionally did analysis on rejection charges in large cities with giant Asian populations.

The explanation may very well be so simple as extra first-generation Asian American candidates wouldn’t have the mandatory documentation to get by means of the mortgage software gauntlet. I have been rejected earlier than as a result of I didn’t have at the least two years of enough freelance revenue after I left my day job in 2012.

At all times refinance your mortgage earlier than leaving your W2 day job please. When you now not have a day job, you might be lifeless to lenders.

For reference, based on Dwelling Mortgage Disclosure Act knowledge, 20% of Black and 15% of Hispanic mortgage candidates had been denied mortgages, in contrast with about 11% of White and 10% of Asian candidates

Answer For Asian Individuals And All Folks With Excessive Credit score Scores

When you do not personal a house but, then your solely plan of action is to grasp what’s occurring and negotiate together with your lender, actual property agent, and vendor. Who is aware of. You would possibly find yourself negotiating so successfully that you find yourself saving much more cash. Too many individuals are too afraid to barter in the case of shopping for a home.

Debtors with excessive credit score scores nonetheless get the bottom mortgage charges and pay the bottom charges. Such debtors will merely have a barely much less whole lot than earlier than. Due to this fact, I would not attempt to recreation the system by purposefully tanking your credit score rating earlier than making use of for a mortgage.

If you’re an Asian American trying to purchase a house, you most likely must get at the least a 760 credit score rating, if not a 800+ credit score rating to have the identical probability of getting an analogous mortgage as different races.

Hold your debt-to-income ratio as little as potential (30% or much less). That is crucial ratio when attempting to get a mortgage or refinance one. When you really feel you might be being handled unfairly, converse up! This manner, you may enhance your probabilities of getting a aggressive mortgage price.

Attempting Tougher Is The Approach

Personally, I welcome the problem to earn extra, enhance my credit score rating, pay down extra debt, and work tougher to care for my household. I’ll educate these classes to my youngsters as properly. Attempting tougher and being financially accountable tends to repay.

On the finish of the day, having the next credit score rating and being in higher monetary form makes life simpler. If different people who find themselves struggling are getting a break, then nice. The quantity of house owner’s fairness householders have collected since 1990 has been huge.

Actual property makes up about 50% of my passive revenue. And passive revenue is what permits my spouse and I to dwell extra freely. I need all people to expertise one of these freedom as quickly as potential.

Since 1999, I’ve additionally been paying a major quantity of taxes annually to assist subsidize the ~50% of working Individuals who don’t pay any federal revenue taxes. Therefore, paying one other a number of thousand {dollars} in greater mortgage charges, if I determine to purchase one other home, will not be an enormous deal.

After considering issues by means of, it seems like an honor to assist others additionally obtain the American dream. I used to be capable of come to America in 1991 for highschool and construct my fortune. I hope many extra individuals get to do the identical as properly.

Reader Questions And Ideas

What are your ideas on the Federal Housing Finance Company charging greater charges for these with greater credit score scores? What are the implications of this new coverage to the housing market? Are you for or in opposition to probably homebuyers with decrease credit score scores attending to pay decrease charges?

Store round on-line for a greater mortgage price with Credible. You will get a number of actual quotes in a single place. One of many keys to getting the bottom mortgage price potential is to get competing affords.

For extra nuanced private finance content material, be a part of 60,000+ others and join the free Monetary Samurai publication and posts by way of e-mail. Monetary Samurai is without doubt one of the largest independently-owned private finance websites that began in 2009.