{kind=link}

Earnings are far more essential, however 401(ok) withdrawals have but to make their mark.

For a lot of causes, we’ve got been trying on the sources of revenue for households ages 62-75 – a bunch eligible for Social Safety, a lot of whom could possibly be presumed to be retired. Three patterns emerged when evaluating information from the Federal Reserve’s 2019 Survey of Shopper Funds (SCF) with the 1995 SCF. Earnings have grow to be more and more essential, revenue from outlined profit plans stays a lot bigger than withdrawals from 401(ok)s, and the distribution of revenue has grow to be extra unequal.

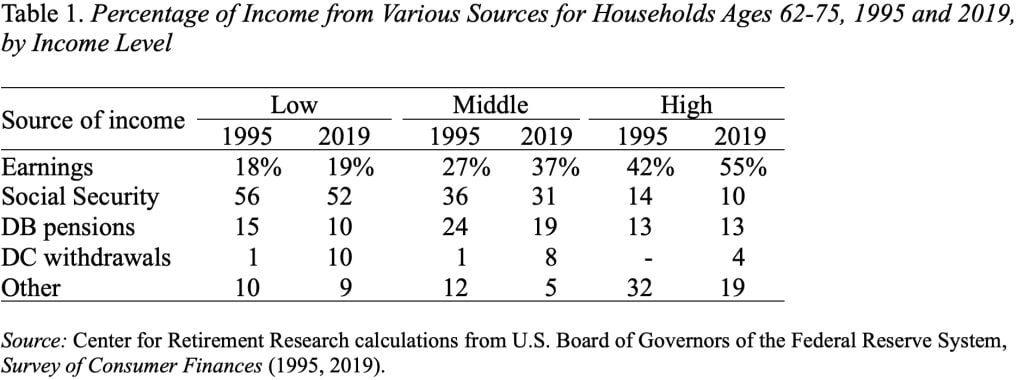

Listed here are the numbers for all households during which the pinnacle is 62-75, grouped by revenue degree. Whereas earnings as a proportion of complete revenue stayed just about fixed for low-income households, earnings elevated by 10 proportion factors for these within the center group and by 13 proportion factors for high-income households (see Desk 1). Within the case of the high-income group, earnings now account for greater than half of all revenue.

The opposite attention-grabbing factor in Desk 1 is the composition of revenue from employer-sponsored retirement plans. We’ve all grow to be accustomed to saying that it’s a 401(ok) world. Certainly, that’s true for immediately’s personal sector employees. However it’s not true but for retirees. Aside from the low-income households, these of retirement age proceed to get considerably extra from outlined profit pensions than from 401(ok) withdrawals. Maybe, this sample shouldn’t be so shocking, provided that: 1) 401(ok)s solely began within the Eighties; 2) solely current retirees can have been capable of spend their entire profession lined by a 401(ok) plan; and three) contributors will not be required to begin drawing down their gathered balances till their early 70s. Furthermore, outlined profit plans stay the key supply of retirement revenue for state and native authorities workers, who comprise about 13 % of the workforce.

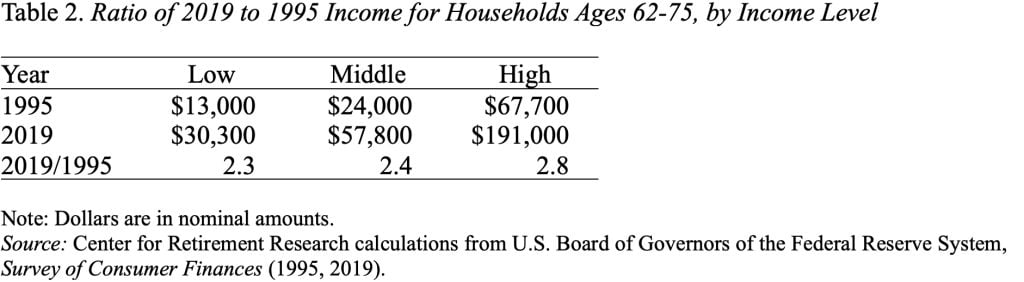

The third level that emerges from these information is that the revenue distribution for these older households has gotten extra unequal (see Desk 2). Excessive-income households’ common revenue in 2019 was 2.8 occasions the 1995 degree, whereas the ratios for low- and middle-income households have been 2.3 and a couple of.4, respectively. The large distinction is earnings. The phrase has gotten out that working longer is the important thing to a safe retirement, and people with essentially the most training and sources have modified their habits.

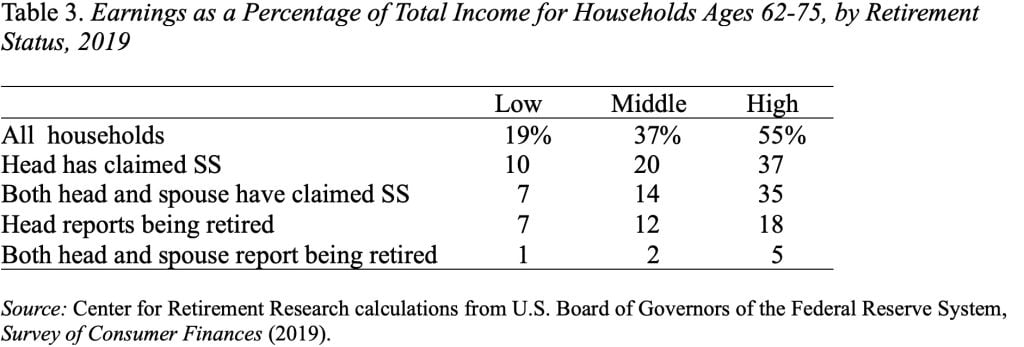

One ultimate situation is that, with the upsurge in earnings, it has gotten more and more laborious to outline “retirement” – notably for high-income households. Receipt of Social Safety (SS) advantages used to look like a surefire strategy to classify a family as retired, however high-income households – even when each spouses have claimed Social Safety – obtain greater than a 3rd of their revenue from earnings (see Desk 3). The one criterion that appears to work – within the sense that earnings are now not essential – is when each the pinnacle and the partner report being retired.

The principle conclusion that emerges from all that is that I’m actually desirous to see the outcomes from the 2022 Survey of Shopper Funds, which ought to come out someday this month.