{kind=link}

Whereas there was some debate concerning the so-called mortgage price lock-in impact, it seems to be a reasonably legit drive within the housing market right now.

Because the logic goes, current owners aren’t shifting as a result of their mortgage charges are so low.

However it’s not solely that they’re so low, it’s additionally the price of substitute, with prevailing market charges now edging nearer to eight%.

So it simply doesn’t make lots of monetary sense for owners to maneuver except they completely should.

And for a lot of, it’s most likely not even doable, thanks to an enormous enhance in prices if exchanging a 3% price for a near-8% price.

Is Mortgage Price Lock-In a Actual Factor?

A brand new survey from Fannie Mae explored mortgage price lock-in and located that whereas it’s definitely a purpose for staying put, it’s not the one purpose.

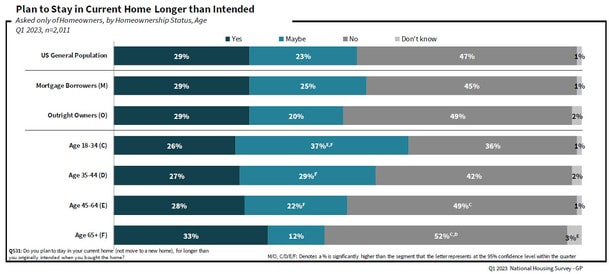

The corporate requested owners by way of their Nationwide Housing Survey in the event that they deliberate to remain of their present properties longer than initially supposed. And in that case, why.

They discovered that an equal 29% share of homeowners with a mortgage (mortgage debtors) and outright homeowners (owners with out a mortgage) deliberate to remain put longer.

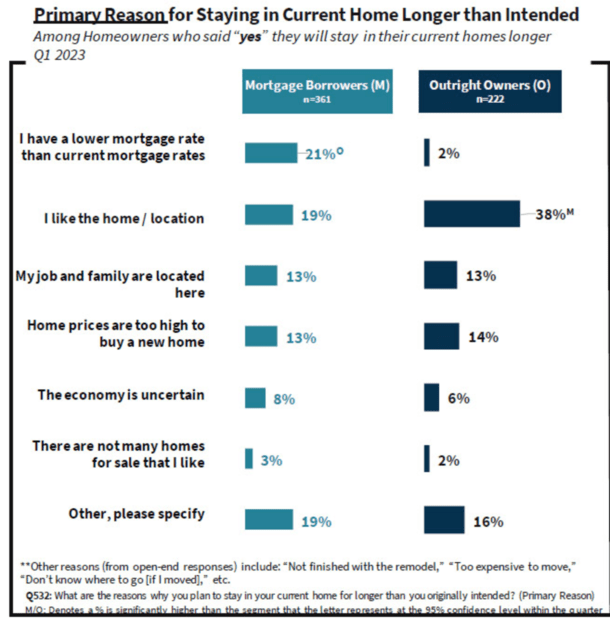

Of the mortgage borrower inhabitants, 21% indicated the choice was primarily as a consequence of having a low mortgage price.

However Fannie factors out that this subset of house owners solely represents 6% of all mortgage debtors.

“These survey outcomes lead us to conclude that there are a number of components contributing to the traditionally low provide of current properties on the market.”

“Whereas the lock-in impact is actual for a lot of customers, the total vary of causes offered by mortgage debtors and outright homeowners for planning to remain of their properties longer paints a considerably extra nuanced image.”

There Are Many Causes Why Housing Tenure Has Elevated, However a Low Mortgage Price Nonetheless Tops the Record

The Fannie Mae researchers argued that even when mortgage charges have been to say no by a significant quantity within the intermediate time period, they might not count on to see a giant surge in for-sale listings.

They imagine there are a “confluence of things and traits contributing to the dearth of housing stock in america,” with the mortgage price lock-in impact one among a number of.

Nonetheless, it did prime the record for these with a mortgage. As you’ll be able to see within the chart above, 21% of house owners with a mortgage cited their decrease mortgage price because the major purpose for staying of their present dwelling longer than supposed.

That was the primary response, although it was trailed pretty carefully by a home-owner merely liking their dwelling/location.

After all, one may argue that it’s simpler to love your private home should you’ve acquired an ultra-low mortgage price connected to it.

And let’s not overlook that these people additionally seemingly acquired in when dwelling costs have been considerably cheaper.

When the 30-year mounted mortgage hit a file low again in 2021, dwelling costs have been additionally loads decrease. In some areas, dwelling values could also be up practically 50% over that point.

So these owners have very low cost housing funds relative to what’s on provide right now, between their smaller mortgage quantity and considerably decrease mortgage price.

In the event you don’t imagine mortgage price performs a task, merely take a look at owners with out a mortgage.

These free and clear debtors are targeted on different issues, like the placement, proximity to job and household.

Mortgage Price Disparity Impacts Everybody, Even Money Patrons

However that doesn’t imply they don’t care about mortgage charges as a result of it’s additionally makes a transfer for them tougher.

Assuming they’ll’t pay for a house with money, they too must face the upper mortgage charges at the moment on provide.

So for them, it could even be “too costly to maneuver,” factoring in a better asking worth and steep mortgage price.

One may additionally blame the dearth of for-sale stock on the disparity between mortgage charges then versus now.

Fewer for-sale listings imply it’s tougher to discover a substitute property. This too may contribute to owners figuring out that they like their current properties extra.

They could possibly be resigned to the truth that shifting is out of query, and/or put extra work into making their current digs higher.

On the finish of the day, you may argue that this speaks extra to the overall lack of affordability in right now’s housing market than the rest.

And till we see extra provide hit the market, it’s not going to alter, even when mortgage charges do come again right down to extra affordable ranges.