{kind=link}

Tens of millions of householders are poised to face larger mortgage charges when their fixed-term loans expire this 12 months – referred to as the “mounted charge cliff”.

The mounted charge cliff refers back to the expiration of fixed-rate phrases on mortgages and their subsequent re-pricing at a lot larger charges, with a brand new report by CoreLogic head of analysis Eliza Owen (pictured above) calling it “one of many greatest potential dangers to housing market values and total stability in 2023”.

The mounted charge cliff – how did we get right here?

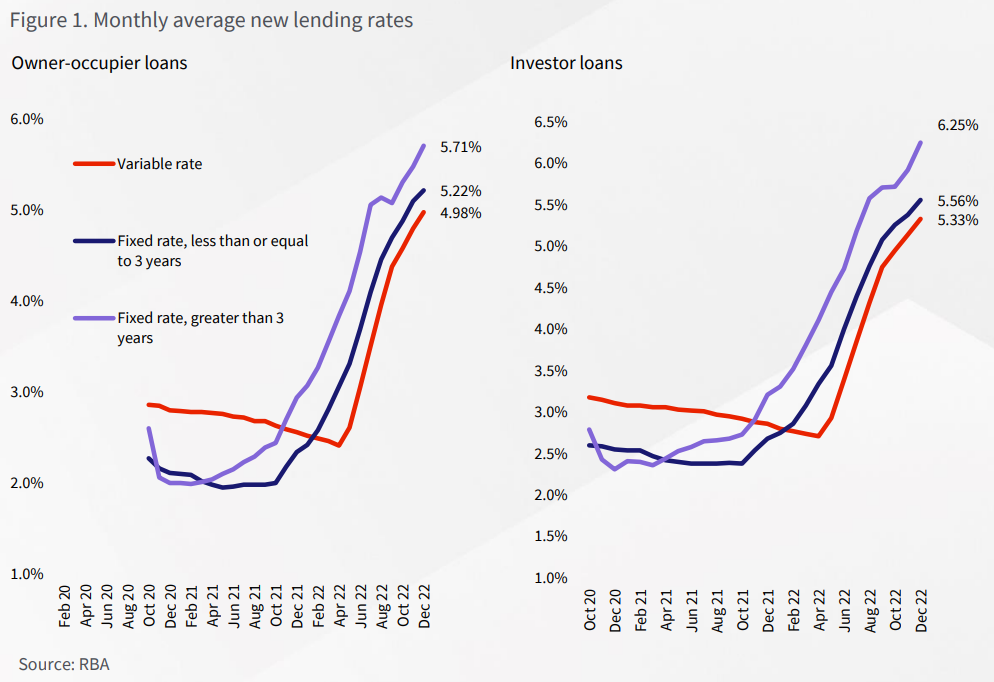

Mortgage charges fell considerably throughout the pandemic, with short-term mounted charges averaging as little as 1.95% in Could 2021 for owner-occupiers. Because of this, fixed-term dwelling lending rose to 46% of recent mortgage commitments in July and August 2021, up from its historic common of 15%.

In its October Monetary Stability Assessment, the RBA famous that about 35% of excellent housing credit score was on mounted phrases, and roughly two-thirds of this debt is ready to run out in 2023.

With the mounted charge interval coming to an finish this 12 months, round 23% of all excellent mounted mortgage debt will probably be repriced at a a lot larger charge, posing a threat to many debtors.

Factoring in one other 50 foundation factors of charge hikes over March and April, common variable charges may very well be round 5.7% for proprietor occupiers and over 6.0% for traders, Owen warned.

What comes subsequent?

The mounted charge cliff will probably be felt most acutely from April 2023, in accordance with Owen, because the change in charges will probably be important as a result of extra charge rises, and common mortgage sizes have grown significantly since April 2021 throughout the housing growth.

The preliminary repricing from a mean two-year mounted time period charge throughout the pandemic to a variable charge two years later will probably be important and can probably pose “some problem to serviceability,” Owen stated, particularly as rates of interest have risen past the three% minimal serviceability buffer really helpful by APRA.

Utilizing the common $538,936 mortgage taken out in April 2021 as a reference level, a set charge of 1.98% will surge to a variable charge of 5.48% in April 2023. This interprets to an added $1,066.63 in month-to-month repayments, going from $1,986.63 underneath a set time period to $3,053.26 underneath a variable charge.

“Stretched serviceability may very well be compounded by a rise within the unemployment charge this 12 months together with larger than budgeted family prices as a result of excessive inflation,” Owen stated.

“An increase in distressed gross sales might additionally put added downward stress on property values. If individuals are pressured to promote their dwelling in a declining market, there may be the added threat of being unable to get better mortgage debt from the sale of a house.”

Amid this looming threat, Owen famous solely 4.9% of lending went out on mounted phrases in December 2022, that means that the majority excellent housing debt will probably be uncovered to fluctuations in rates of interest by the tip of 2023, as many fixed-term loans may have expired.

“On one hand, this will increase the chance of decreased serviceability as rates of interest rise,” she stated. “Then again, debtors could also be higher positioned to hunt a decrease rate of interest because the money charge passes a peak, which some imagine may very well be as quickly as late 2023.”

Owen pointed to a current report from CBA highlighting that the RBA may have to start out lowering charges by the fourth quarter of 2023 with the intention to keep away from a recession.

“This implies whereas elevated variable charges might create robust situations for households within the quick time period, the steep hike in curiosity repayments won’t be for the whole lifetime of the mortgage,” she stated. “With exterior refinancing hovering round report highs, banks may even be extra incentivised to scale back their mortgage charge choices to remain aggressive.”

Owen’s evaluation additionally reveals that fairness stays excessive in most markets regardless of the current decline in dwelling values in Australia.

Whereas the decline in Australia’s housing markets from respective peaks is extremely diversified, CoreLogic has estimated that solely 2.9% of suburbs throughout the nation have seen dwelling values fall greater than 20% from their current peak.

“Giant deposits additionally assist to strengthen the fairness place of mortgage holders,” Owen stated. “RBA assistant governor Brad Jones not too long ago famous that round 0.5% of dwelling loans have been in unfavourable fairness amid present value falls. If dwelling values have been to fall an extra 10%, the RBA estimates the speed of loans in unfavourable fairness would solely rise to round 1%.”

What’s the extent of the influence?

General, Owen stated there may be presently no information to point any important influence on the housing market, and it might take a while for the results to turn out to be obvious.

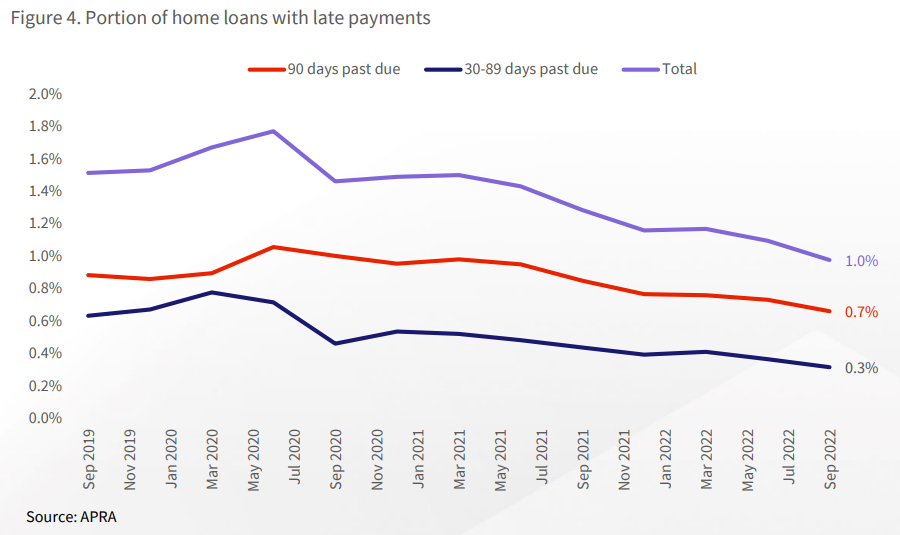

She referred to APRA’s newest accessible information on non-performing loans from September 2022, which indicated that only one.0% of dwelling loans have been at the least 30 days overdue. This quantity has additionally been falling, however the accessible information has solely captured round two-thirds of the rate of interest will increase which have been seen up to now.

Understanding the influence of rising charges on households might be tough as a result of totally different revenue cohorts and help networks will reply otherwise to larger curiosity prices, Owen stated.

For instance, some individuals might be able to transfer in with their mother and father and lease out their dwelling to complement mortgage funds, whereas others on larger incomes can usually afford to allocate the next portion of their revenue to housing.

Establishments comparable to banks may even be working proactively to keep away from mass mortgage defaults within the housing market, and should implement short-term forbearance measures comparable to extending the mortgage time period, quickly reverting to interest-only repayments, or lowering month-to-month repayments.

The implementation of mortgage reimbursement holidays on the onset of the pandemic had equally seen “the rise of a ‘cliff’ narrative” because the deadline approached, Owen stated, however banks prolonged the deadline and there gave the impression to be no important influence on the property market when the deferrals ended. Nonetheless, she acknowledged that “the financial and housing worth context was starkly totally different then, to what it’s now.”

“Trying forward, there’s no escaping that Australians with fixed-rate loans are about to see a painful adjustment,” Owen added. “That is partly the intention of rising charges, as households must curb spending in response to larger curiosity prices. Thus far, listings information and arrears information counsel there may be minimal influence on the housing market from defaults. Nevertheless, the true take a look at of the market will probably be over the following ten months.”