{kind=link}

Whereas owners have definitely felt the affect of 12 money charge will increase in 13 months, new information has revealed that banks have been comparatively restrained, not passing on the entire Reserve Financial institution’s official money charge will increase over the previous yr.

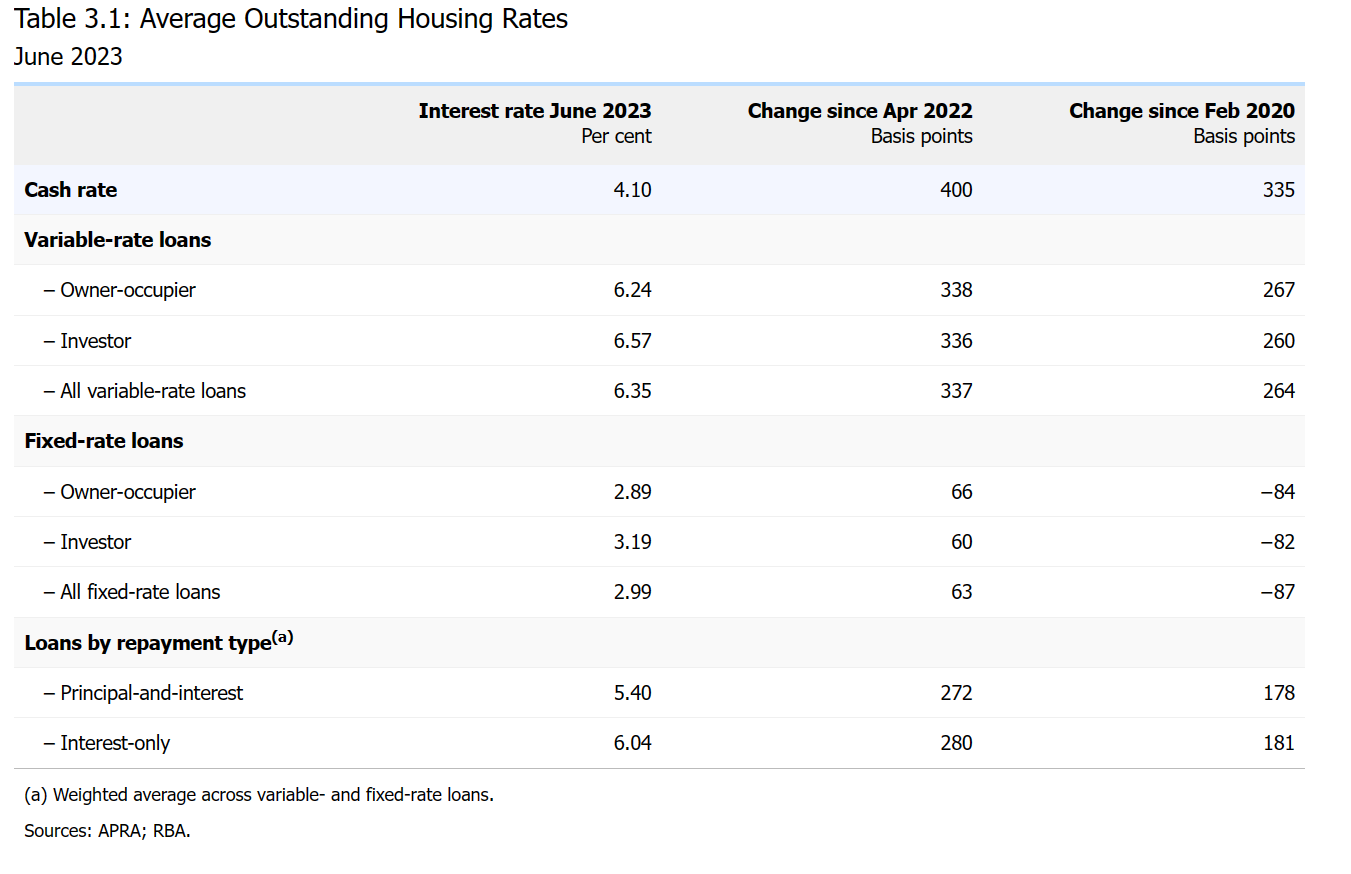

The RBA elevated the money charge by 400 foundation factors between April 2022 and June 2023, from 0.10% to 4.10%. Nevertheless, lenders solely elevated their variable charges by a mean of solely 337 foundation factors.

Which means that owners might be going through charges which can be practically 16% increased throughout the board if the banks had strictly adopted the OCR.

So why is that this? Effectively, the Reserve Financial institution places it right down to “sturdy competitors within the mortgage market.”

Benjamin Cooper (pictured above), a mortgage dealer from Sydney’s Shore Monetary, mentioned mortgage brokers performed a central function in fostering this competitors, by serving to customers examine loans from many various lenders.

“As a mortgage dealer, you might have relationships with the BDMs of the banks which permits for small, and essential reductions on charges for the purchasers,” Cooper mentioned. “We even have expertise permitting us to see the perfect charges and merchandise obtainable for the purchasers, which in flip places stress on the banks and BDMs to have the bottom charges.”

A brand new charge cycle

The break up between the OCR and the speed at which lenders raised charges was much more stark over an extended interval.

Since February 2020, when the OCR was on the then-record low of 0.75%, the official money charge has risen 335 foundation factors to June whereas lenders solely elevated variable charge loans by 264 foundation factors, representing a 22.6% distinction.

This was roughly constant throughout each investor and owner-occupier variable charge loans.

Nevertheless, in current months, there are indications that competitors within the housing mortgage market has change into much less intense.

Particularly, the typical variable charge on new housing loans rose by 29 foundation factors in June, in line with the RBA. This improve surpassed the rise within the money charge, marking a noteworthy improvement throughout this era of tightening.

Additionally, lenders have lowered reductions on their marketed lending charges, and most have now withdrawn cashback gives for brand spanking new or refinancing debtors.

From a document excessive of 35 lenders providing cashback offers in March 2023, it has dwindled down to simply 15 in July.

Out of the foremost banks, solely ANZ continues to be sticking with a cashback deal, with a $3,000 cashback supply for first house patrons with loans of $250,000 or extra, in line with Canstar’s August information.

Whereas inflation continues to be above the RBA’s goal band and Reserve Financial institution governor Philip Lowe indicating that additional tightening of financial coverage could also be required within the newest money charge announcement, forecasts have gotten cautiously optimistic that the top of the speed mountaineering cycle is close to.

Cooper mentioned that with nearly all of banks beginning to ease off on charge rises, it was an indication that the market had “reached the height” or was “very shut” to the top of the rises.

Rolling off document low mounted charges

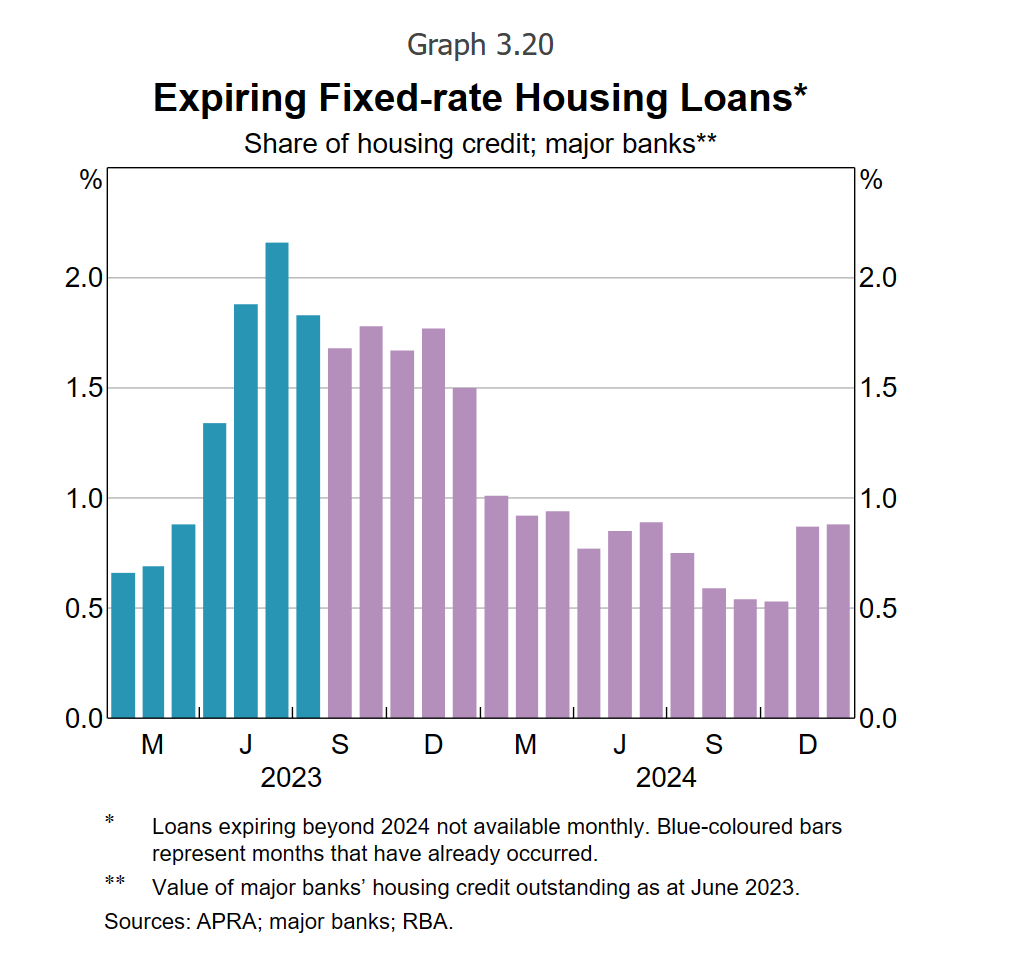

Whereas the indicators level to an easing of variable charges, there may be nonetheless extra ache forward for these on mounted charges who’re more and more affected by mortgage stress.

General, common excellent mortgage charge has elevated by round 275 foundation factors since Could 2022, 125 foundation factors lower than the money charge, in line with the RBA. This divergence largely displays the excessive share of fixed-rate housing loans which can be nonetheless excellent.

The RBA mentioned that the share of debtors rolling off fixed-rate mortgages – taken out two to a few years in the past at low rates of interest – onto a lot increased charges peaked at slightly below 5.5% of excellent housing credit score within the June quarter.

The central financial institution forecasts this to remain excessive for the remainder of the yr, peaking between July and December earlier than declining in 2024.

As these expiries happen, a bigger portion of debtors will expertise the affect of the rise within the money charge since Could 2022, resulting in a continued rise within the common excellent mortgage charge.

Nonetheless, in line with Cooper, the method would be the identical for brokers.

“Maintain these relationships sturdy with the BDMs and work with them to cut back the carded charges alongside their pricing groups,” he mentioned. “And contact base together with your purchasers as a lot as you may to information them via this surroundings.”

What do you consider this concern? Remark under.