{kind=link}

U.S. Efficiency

March concluded with an uptick in weekly U.S. lodge occupancy, which reached the second highest degree of the yr (66.2%), up 2.2 share factors (ppts) from a yr in the past, however 1.3 share factors beneath the year-to-date (YTD) excessive achieved two weeks in the past. Common day by day fee (ADR) of US$158 matched final week’s degree and like occupancy, it was the second highest of the yr to date. Extra importantly, ADR elevated 7.3% yr over yr (YoY), forward of inflation (+6%). Income per out there room (RevPAR) got here in at US$105, up 10.9% YoY and 14% increased than 2019. Actual (inflation-adjusted) ADR was basically matched the 2019 degree whereas actual RevPAR was down 4%.

High 25 Market occupancy and ADR typically adopted the identical sample because the U.S. total, with occupancy rising to 72.8% from 72.3% every week in the past. In comparison with final yr, occupancy was up 4ppts YoY – its largest acquire of the previous three weeks. It ought to be famous that the occupancy degree for the High 25 Markets has been above 72% for the previous 4 weeks – its longest streak at that degree since October.

Weekly ADR in these key markets grew 9.0% YoY, its second week beneath double-digit progress as simple Omicron comparisons fade away, however the progress fee was nonetheless increased than the speed of inflation. With robust will increase in each occupancy and ADR, RevPAR jumped 15.4%, a tempo that was almost double the expansion seen every week in the past.

Whereas every day of the week noticed occupancy and demand progress week over week, weekdays (Monday-Wednesday) drove High 25 Market progress as enterprise and group journey continued its restoration. These three days accounted for 60% of the year-over-year acquire in weekly room demand. Weekday occupancy elevated 5.9ppts YoY to 71.5% and has been above 71% for the previous 4 weeks, though this week’s end result was the bottom of the 4. A yr in the past, and through this similar time interval, weekday occupancy failed to interrupt 70%.

All the High 25 Markets, minus Atlanta and Miami, noticed year-over-year progress in weekday room demand. The biggest contributors have been Las Vegas and Washington, D.C., which noticed its highest weekday occupancy (83%) because the begin of the pandemic. The market additionally had its highest weekly occupancy (78.8%) courtesy of the annual Nationwide Cherry Blossom Pageant. This yr’s weekly occupancy was the tenth highest since 2000. Compared, the 2019 degree for a similar week ranked ninth (79.9%).

Exterior of the High 25 Markets, weekly occupancy (62.5%, +1.1 ppts) and ADR (US$138, +5.1%) are enhancing at a slower tempo, which is predicted given their substantial restoration within the prior two years. Weekly RevPAR was up 7.0% YoY to US$86.

After falling for 5 consecutive weeks, U.S. weekend occupancy elevated 1ppt YoY to 75.6%, its highest degree of the yr to date. The acquire was pushed by the High 25 Markets, the place occupancy grew 2.4ppts to 81.1% – its highest degree because the fall. Exterior the High 25, occupancy was comparatively flat (72.6%, +0.2ppts YoY).

Six of 167 STR-defined U.S. markets reported occupancy above 80%, with the highest three spots occurring in High 25 Markets. One other 37 markets total noticed occupancy between 70% and 80%. In complete, two-thirds (110 markets) reported occupancy at or above 60% for the week, rising from 99 markets final week. A yr in the past, 98 markets reached 60% occupancy for the matched week, whereas 121 markets had hit (or beat) that weekly benchmark in 2019. Some prime occupancy callouts which replicate the influence of conventions, strong spring journey and sports activities tournaments embody:

- Highest in High 25: Las Vegas (86.1%), Tampa (82.1%), and Nashville (82%)

- Highest in Non-High 25: Florida Keys (82.8%), Sarasota (81.2%), and Ft. Lauderdale (80.8%)

- High YoY gainers: Louisville (+20ppts), Indianapolis (+13ppts), and Washington, D.C. (+12ppts),

When it comes to weekly RevPAR good points, 5 of the High 25 markets had double-digit WoW RevPAR share will increase above the prior week: Houston (+23%), Saint Louis (+19%), Washington, D.C. (+18%), Las Vegas (+13%), and Nashville (+11%). Thirty-seven markets noticed WoW RevPAR will increase of 10% or increased in comparison with a complete of 19 markets with a double-digit elevate within the prior week. RevPAR callouts embody:

- Highest High 25 RevPAR: Oahu (US$222), Miami (US$218), NYC (US$195), and Orlando (US$191).

- Highest non-High 25 RevPAR: Maui (US$491), Florida Keys (US$407), and Hawaii/Kauai Islands (US$354).

- High WoW gainers: Indianapolis (+31%), Augusta (+31%), and Tulsa (+29%).

- High YoY gainers: Louisville (+92%), Indianapolis (+53%), Washington, D.C. (+44%), and Houston (+42%), which hosted the NCAA Remaining 4 event.

World Efficiency

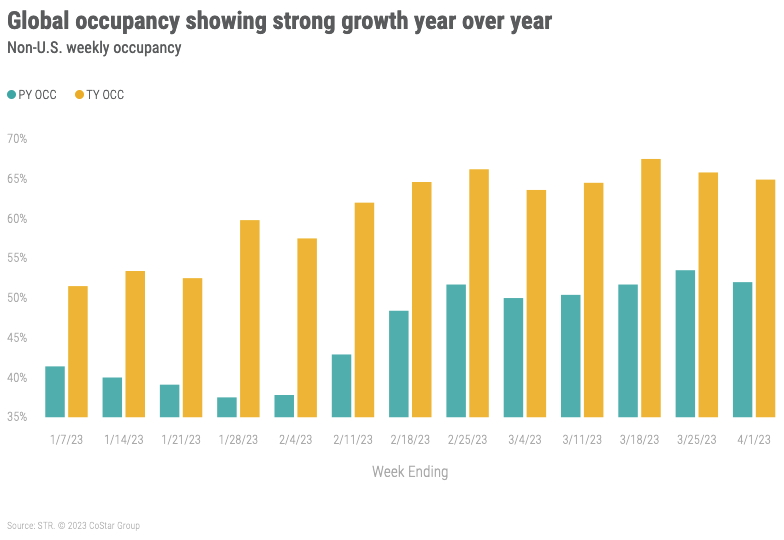

World occupancy outdoors the U.S. declined barely this week to 64.9%, down 0.9ppts from final week however 13ppts forward of final yr. This week’s occupancy was the 14th highest because the begin of the pandemic. Weekly ADR rose 20.5% YoY to US$134. With robust leads to each occupancy and ADR, RevPAR elevated by 50.8% YoY to US$87. RevPAR has grown by 50% or extra each week this yr, besides one (the week ending 25 March). As well as, each ADR and RevPAR attained their highest ranges of the previous 12 weeks.

Among the many prime 10 nations primarily based on provide, occupancy was up sharply (+17.4ppts YoY) led by China (+31.5ppts YoY) and adopted by Italy, Germany, and Japan the place occupancy good points have been within the mid-teens yr over yr. Indonesia noticed a noticeable lower (-8.4ppts YoY) because of the second week of Ramadan. All 10 nations noticed YoY ADR progress led by Japan, the place ADR jumped greater than 106% YoY, which led to a 158% YoY acquire in RevPAR. China additionally noticed very robust RevPAR progress, up 151% YoY. Collectively, weekly RevPAR within the prime nations was up 62.7% YoY.

Globally, weekly occupancy was the best within the Bahamas (80.5%) adopted by Eire (79.6%), and Jamaica (79.5%). Fifteen of the 103 nations tracked weekly reported occupancy above 70% this week, which was lower than the 27 that did so every week in the past.

Remaining ideas

This was one other strong week with demand barely outpacing our expectations. Weekday journey continued to get well, driving progress within the High 25 U.S. markets. We’re additionally inspired by the robust year-over-year progress within the prime 10 nations excluding the U.S. Within the U.S., the trade is coming into a interval of weekly volatility, that in-between interval as spring break journey wraps up and summer season journey nears. Nonetheless, these subsequent few weeks will proceed to see restoration in weekday demand from enterprise and group segments.

Trying forward

Our prediction for subsequent week is for slower demand with much less optimistic efficiency within the High 25 Markets and usually flat efficiency coming from markets outdoors the High 25. An identical prediction is held globally the place the big markets will present muted efficiency whereas extra leisure locations will stay regular.

This text initially appeared on STR.